Historic Stories

One of the unexpected benefits of ManhattanLife’s -year legacy is finding its treasure trove of stories, historical milestones and industry firsts. Not only are they interesting, they also validate the persona of our company. We invite you to learn more about ManhattanLife and the journey that led us to where we are today. And don’t forget to check back to learn more as we discover new stories to share!

MANHATTANLIFE STORIES:

1850 to At A Glance

Years of ManhattanLife

The 2019 rebranding of ManhattanLife projects a company that has always been keenly focused on the wellbeing of its policyholders, expressed through its service, innovation and independence. The Company’s -year history is rich with stories both human interest and industry related that have demonstrated this commitment time and time again.

To provide a visual snapshot of this track record, a graphic timeline was created documenting milestones that reflect ManhattanLife’s values, including such notable events as commissioning America’s first skyscraper in 1894 and electing a woman to their Board of Directors in 1972. Click here to see the ManhattanLife graphic timeline of dynamic events spanning 1850 through .

MANHATTANLIFE STORIES:

ManhattanLife and The Steinway

At Home with The Arts

Throughout its history, ManhattanLife has had an intriguing relationship with the structures and spaces that have housed its business. The Company commissioned the country's first skyscraper in 1892 and its current headquarters in Houston is home to a museum-worthy collection of works on paper, curated personally by ManhattanLife’s owner David Harris.

This is the story of 111 West 57th street in New York City, which served as the Company's HQ from 1958 to 1978. It all started in March of 1958 when three members of the Board of Directors assigned with procuring a larger space for the growing company achieved approval to purchase the original headquarters of legendary piano manufacturer, Steinway & Sons.

{kind=link}

Commanding Cityscapes

With the acquisition of 111 West 57th, The Company renamed the structure “The Manhattan Building” and branded it by installing a relief on its façade of the year of its founding, 1850, and the Statue of Liberty — a feature of the Manhattanlife corporate identity. The 16-story building had 160,000 square feet of space including upper floors dedicated to a musical headquarters with studios for artists and teachers. The Steinway & Sons 32,000 square foot grand showroom remained in the building’s basement, ground floor, 2nd floor and part of the 4th floor. The popular building received media attention and was honored by The Fifth Avenue Association with a Gold Medal Award for best construction in the Fifth Avenue district.

A Space to Thrive

ManhattanLife’s leadership at the time kept the building’s tenants on short leases in anticipation of hiring additional personnel to accommodate the Company’s continued growth. Always evolving its product portfolio and advancing its business practices, the Company achieved some compelling “firsts” during this Steinway era. It introduced the industry’s first pre-authorized monthly premium check plan with the “Man-O-Matic.” It published the “You and The Manhattan Life” employee handbook and presented it to every employee in 1959. And in 1963 the Company entered the digital age, contracting General Electric for the delivery of the 225 Computer.

The Tower of Tomorrow

The Steinway Building is still making news today. Now known as “Steinway Tower” 111 West 57th is currently being developed for residential use. Upon completion, its futuristic design will boast 84 stories, making it one of the tallest buildings in the United States. It will also be the thinnest skyscraper in the world, with a width-to-height ratio of about 1:23 to 1:24. Steinway Tower is scheduled to formally launch in late 2020.

MANHATTANLIFE STORIES:

THE INDEPENDENT

Operating According to Its Mission

Within an industry peer group comprised primarily of large, publicly traded companies, ManhattanLife owns a differentiated position as an independent.

Private and closely held by choice, ManhattanLife is free to make decisions that align with its stated values and core mission — helping policyholders, producers and employees with attaining and sustaining health, wealth and security throughout their lives.

A potential conflict of interest exists within an organization that is beholden to investors and analysts on one hand and policyholders and producers on the other. At best, the required focus on quarterly earnings is a distraction from servicing policies and innovating products. At worst, it could mean prioritizing preserving shareholder value over advocating on behalf of policyholders.

A History of Independence

ManhattanLife has a storied history of conducting business its own way. Founded in 1850, this independent is one of the industry’s oldest insurance companies, has survived multiple wars, plagues, the Great Depression and the Great Recession, and has done so without compromising its values or determination to “do the right thing.” Even when pressured not to.

This was demonstrated early in the Company’s history when the Civil War ended and ManhattanLife sought out the surviving policyholders of the South in order to fulfill their claims. In spite of the federal government’s prevailing opinion that they ignore these claims, ManhattanLife honored the claims because it believed it was morally the right thing to do.

Free to Create and Innovate

Being an independent can also be about “independence from” — independence from rigidity of thinking, the status quo and herd mentality. This allows ManhattanLife to focus on what matters most — improving upon its product offering and rewarding its valued relationships with producers. The Company embraces the kind of nimbleness, creativity and generosity of spirit that generally cannot thrive within the bureaucratic confines of the large publicly traded insurance companies, known within the industry as “the Bigs”.

With years of independently growing its business, today ManhattanLife plays in the space of the market leaders. Yet, as an independent, the Company remains the true alternative offering product breadth and financial strength that can go toe-to-toe with other top carriers. ManhattanLife — all the benefits of the Bigs but better.

MANHATTANLIFE STORIES:

America's First Skyscraper

Trailblazers by Design

The history of New York City’s skyline is almost as rich as the city itself. And at the heart of this history rests the ManhattanLife building — the first skyscraper to be designed and constructed in the United States.

Reaching New Heights

The development of the ManhattanLife building began in 1892, when The Company commissioned architecture firm Kimball & Thompson for its design, which would tower 347 feet above Broadway, and 400 feet above the foundation. Such heights had never been reached, so to achieve this, a new type of construction was required – a caisson-type foundation. This design – the first caisson-type foundation used in New York – is commonplace today, but at the time it was considered a revolutionary approach to minimizing the risk of damage to surrounding buildings.

At first, the Commissioner of Buildings was resistant to permitting the groundbreaking structure, but eventually consented asking only that the lead architect George Kramer Thompson give his word that it would work.

A herculean effort, the skyscraper was completed in 12 months and 27 days with no lives lost during its construction. It was reported that enough steel was used in the building to install 100 miles of railroad.

The Talk of the Town

Throughout its development, the ManhattanLife building became a topic of discussion in the newspapers and magazines of the time. Truly innovative, this project captured the interest of New York’s media and citizens, and was called an attempt to “push dem clouds away” as the Insurance Record reported.

{kind=link}

The Company moved into its cutting-edge headquarters in 1894 and the building quickly became one of New York’s prime sight seeing attractions, much like the Empire State Building or Radio City Music Hall of today. Guides were available to lead visitors through the nation’s first skyscraper, including the structure’s tower occupied by the Government Weather Station.

A newsworthy moment during the building’s development is tied to the World’s Fair. The Insurance Advocate noted editorially at the time of the fair at the Art Palace that, “ManhattanLife made a good hit when it conceived the idea of exhibiting a model of its elegant new building, now in the course of construction, at the World’s Fair. While taking in the sights of the wonderful exposition, we were convinced of this fact by observing a large number of people admiring that colossal piece of architecture. For The ManhattanLife it is an advertisement par excellence.”

MANHATTANLIFE STORIES:

The Old Reliable

From Young Resilient to Old Reliable

In its eleventh year in business, the ManhattanLife insurance company was thriving despite strenuous circumstances. Its team of field agents had grown to 464, with representation expanding from New York to across the country as far as California and Texas. With assets over $1 million, The Company had persevered through the Yellow Fever Epidemic of 1853 and the Panic of 1857 which had resulted in the suspension of New York City banks. However, it would soon face its greatest challenge, and an epic and defining milestone, with the attack on Fort Sumter on March 12, 1861 and the resulting four years of Civil War.

Operating During War Time

The battle between the North and South presented operational challenges to The Company, which a special meeting of the Board was called to address. ManhattanLife’s field force in the North needed to increase to compensate for the loss of business in the South due to the war. There was also the issue of granting permits to policyholders volunteering for Union military or naval service. The Board voted to grant permits at adjusted rates provided they made applications within 10 days of entering service. Policyholders not wishing to pay the extra premium for war risk were allowed to let the policies lapse with the provision they would be reinstated at the end of the war with their demonstration of good health.

A Moral Versus Legal Interpretation

Operating during wartime presented philosophical challenges as well. The Company’s Claims Committee had to weigh the question of whether to honor claims based on a moral evaluation rather than a purely legalistic interpretation. Some Board members expressed the opinion that insured policyholders had not taken ordinary precaution in the payment of war premiums without a permit from The Company and therefore were not eligible to make a claim. Upon review, the Directors eventually discerned that the servicemen had acted in good faith and given their lives to their country, leaving their families in financial hardship. The decision was made to honor these claims, a motion proving ManhattanLife’s leadership were men of compassion.

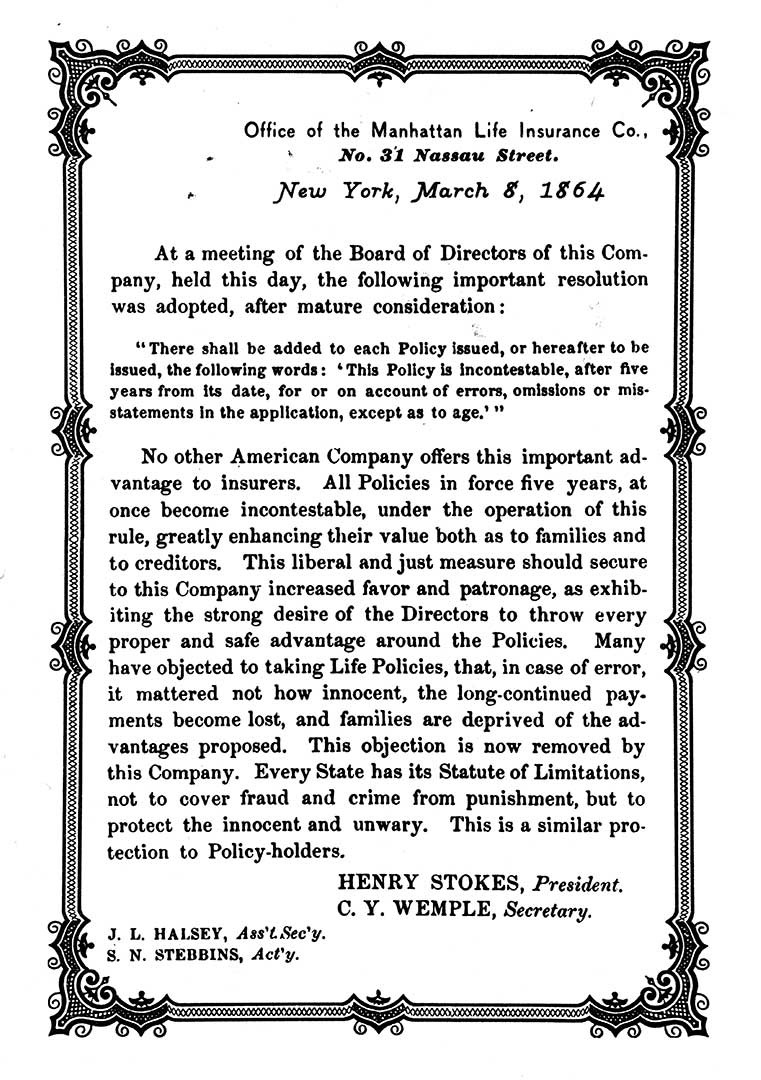

Introducing Incontestability

In 1863, an incontestability clause was introduced to ManhattanLife’s Applications Committee for consideration. The clause would essentially eliminate potential loopholes and ensure The Company’s accountability to policyholders. The motion was seconded but lost on a vote. A champion for the clause, the Chairman of ManhattanLife’s Claims Committee reintroduced it citing both the advantages and objections to the policy feature as well as its success in the practice of European insurance companies. To date, no American insurance company had ever offered policyholders the protection of incontestability. The key language in the clause read “This policy is incontestable, after five years from its date, for or on account of errors, omission, or misstatements in the application, except as to age.” The motion passed and a copy of the resolution was sent to all policyholders and the clause was included in all future policies.

{kind=link}

Post War Restoration and Restitution

In the spring of 1865 following the end of the Civil War and the assassination of President Abraham Lincoln, ManhattanLife set about two major initiatives — reestablishing its Southern agencies and searching out the Southern policyholders and beneficiaries with whom The Company had lost contact during the time of war. Communications and monetary transactions across battle lines were mostly suspended therefore policyholders were unable to pay their premiums. Legally, the policies were considered lapsed. ManhattanLife could either rigidly abide by the terms of its contracts, or, take a liberal rather than legal view and pay the claims minus the amount of unpaid premiums. It chose the latter, and soon word spread throughout the South earning the Company the moniker of “The Old Reliable”. And as ManhattanLife reestablished its presence in Virginia, Kentucky, Georgia, Mississippi, Alabama, Louisiana and Texas, agents found this compassionate approach to claim settlements and policy reinstatement and the earned reputation of reliability were some of The Company’s most valuable assets.

ManhattanLife’s founding Directors unanimously agreed The Company should always operate according to the good faith interpretation of its word — not just the minimum of what was contractually required. Whether making decisions based on what is believed to be morally right or implementing a self-governing clause to protect policyholders — fairness and reliability have consistently been cornerstones of the ManhattanLife brand throughout its -year history and today. It is this demonstrated core value that has inspired The Company’s positioning line — Standing by You. Since 1850.